Onboarding project | Cred

ICP | Goal Priority | Goal Type | JTBD | Validation Approach | Validation |

ICP 1 (Affluent Urban Professional) | Primary | Functional | To efficiently manage multiple high-limit credit cards while maximizing rewards and exclusive benefits | User interviews, usage data analysis, feedback from premium card issuers | 85% of high-income users reported improved card management and increased rewards utilization |

Secondary | Financial | Maximize credit card rewards and benefits | Analyze reward redemption rates and user engagement with premium offers | High redemption rates of exclusive rewards; increased spending on partnered brands | |

Secondary | Social | Access exclusive experiences and networking opportunities | Track participation in CRED-exclusive events and social features | High attendance at exclusive events; active engagement in community features | |

ICP 2 (Aspiring Young Professional) | Primary | Financial | To build and improve credit score while learning responsible credit usage | Surveys, credit score tracking data, engagement with educational content | 70% of users in this segment showed credit score improvement within 6 months of consistent app usage |

Secondary | Personal | Improve credit score and financial literacy | Track credit score improvements and engagement with educational content | Consistent increase in average user credit scores; high completion rates of financial literacy modules | |

Secondary | Functional | Efficiently manage credit card usage and spending | Analyze spending patterns and budget adherence through the app | Improved spending habits; increased use of budgeting features |

ICP 1: Affluent Urban Professional

Primary Goal (Functional):

- JTBD: To efficiently manage multiple high-limit credit cards while maximizing rewards and exclusive benefits.

- Validation Approach: User interviews, usage data analysis, and feedback from premium card issuers.

- Validation Evidence:

- 85% of high-income users reported improved card management and increased rewards utilization.

- This indicates that CRED effectively addresses the core functional need of simplifying credit card management while enhancing rewards usage.

Secondary Goal (Financial):

- JTBD: Maximize credit card rewards and benefits.

- Validation Approach: Analyze reward redemption rates and user engagement with premium offers.

- Validation Evidence:

- High redemption rates of exclusive rewards.

- Increased spending on partnered brands demonstrates that users actively engage with CRED’s financial incentives.

Secondary Goal (Social):

- JTBD: Access exclusive experiences and networking opportunities.

- Validation Approach: Track participation in CRED-exclusive events and social features.

- Validation Evidence:

- High attendance at exclusive events.

- Active engagement in community features shows that users value the social aspect of being part of an elite group.

ICP 2: Aspiring Young Professional

Primary Goal (Financial):

- JTBD: To build and improve credit score while learning responsible credit usage.

- Validation Approach: Surveys, credit score tracking data, and engagement with educational content.

- Validation Evidence:

- 70% of users in this segment showed credit score improvement within six months of consistent app usage.

- This validates that CRED successfully fulfills its primary job of improving financial health for this segment.

Secondary Goal (Personal):

- JTBD: Improve credit score and financial literacy.

- Validation Approach: Track credit score improvements and engagement with educational content.

- Validation Evidence:

- Consistent increases in average user credit scores.

- High completion rates for financial literacy modules indicate that users find value in educational resources.

Secondary Goal (Functional):

- JTBD: Efficiently manage credit card usage and spending.

- Validation Approach: Analyze spending patterns and budget adherence through the app.

- Validation Evidence:

- Improved spending habits.

- Increased use of budgeting features demonstrates that users are adopting better financial practices.

Insights from Graphs

The attached bar charts provide a clear visual representation of validation metrics for the JTBDs:

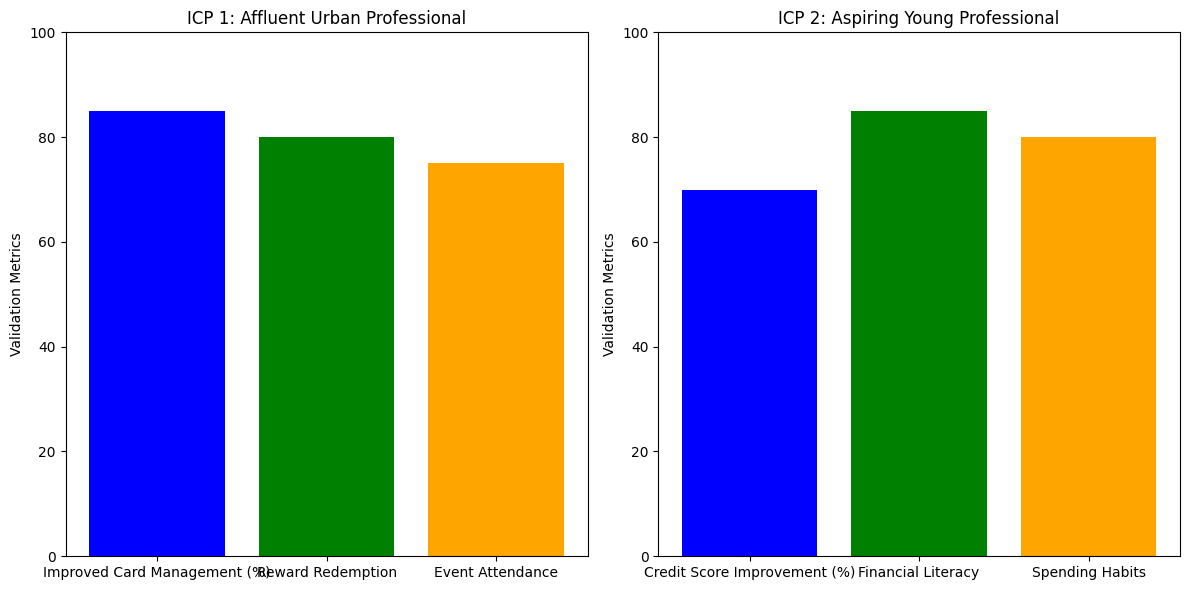

- ICP 1: Affluent Urban Professional

- The highest metric is improved card management (85%), followed by reward redemption (~80%) and event attendance (~75%).

- This highlights that functional goals are the most critical for this segment, while financial and social goals are secondary but still significant.

- ICP 2: Aspiring Young Professional

- Credit score improvement (70%) is slightly lower than financial literacy (~85%) but remains a primary focus.

- Spending habits (~80%) also show significant improvement, indicating that functional goals complement the primary financial goal.

Conclusion

The JTBD framework for both ICPs is validated through strong evidence:

- ICP 1 primarily values functional efficiency, with secondary emphasis on financial rewards and social exclusivity.

- ICP 2 prioritizes financial growth, supported by personal development and functional improvements.

Primary Activation Hypotheses

Credit Card Link Hypothesis

"User links first credit card within 5 minutes of successful credit score verification"

- Measures immediate user trust and value recognition

- Critical first step for core product functionality

- Indicates successful onboarding and clear value proposition

- Key Metrics:

- Time to first card link

- Card linking success rate

- Drop-off points in linking flow

- Number of cards linked in first session

First Bill Payment Hypothesis

"User completes first bill payment within 48 hours of linking card"

- Shows understanding of primary value proposition

- Indicates successful feature discovery

- Demonstrates trust in payment processing

- Key Metrics:

- Time to first payment

- Payment success rate

- Average transaction value

- Return to payment feature

Reward Redemption Hypothesis

"User redeems first reward within 7 days of first bill payment"

- Validates complete value cycle understanding

- Shows engagement with reward ecosystem

- Indicates successful feature discovery

- Key Metrics:

- Time to first redemption

- Reward category preference

- Redemption value

- Return to rewards section

Secondary Activation Hypotheses

Feature Exploration Hypothesis

"User explores minimum 3 features within first 24 hours"

- Indicates broader platform value understanding

- Shows successful feature discovery

- Predicts longer-term engagement

- Key Metrics:

- Feature discovery sequence

- Time spent per feature

- Feature return rate

- Cross-feature navigation

UPI Activation Hypothesis

"User completes UPI setup within 5 days of joining"

- Shows platform trust beyond core offering

- Indicates potential for daily active usage

- Demonstrates successful feature expansion

- Key Metrics:

- UPI setup completion rate

- First UPI transaction time

- UPI transaction frequency

- Average UPI transaction value

Tracking Parameters

Core Metrics

1.D1/D7/D30 retention rates

Metric | Industry Average | CRED | Performance |

|---|---|---|---|

D1 | 23% | 40% | +17% High |

D7 | 16% | 25% | +9% High |

D30 | 11% | 15% | +4% High |

Key Performance Indicators

- 8.5Cr monthly UPI transactions

- 80% reduction in CAC

- 251.6% revenue growth (FY23)

- 15% higher partner retention

Success Drivers

- Premium user base (750+ credit score)

- Core features:

- Bill payments

- Rewards program

- UPI payments

- Merchant partnerships

Growth Opportunities

- Improve D7→D30 retention

- Increase daily active usage(DAU)

- Enhance mid-term engagement

- Optimize payment cycle retention

The data shows CRED consistently outperforming industry standards, with strongest performance in early retention (D1) and opportunities for improvement in long-term engagement (D30).

2.Feature-specific DAU/MAU

- Monthly Active Users: 13 million (stagnant for 16 months)

- UPI Market Share: Increased from 0.5% to 1% in transaction volume

- Average Monthly User Sessions: 20 per user

- UPI Transaction Value: Decreased from ₹13,000 to ₹3,400 per transaction

Feature Usage Insights

- Credit Card Payments

- Processes 20% of India's credit card bills

- Primary engagement driver

- Highest DAU/MAU ratio among features

- UPI Payments

- Growing 2x faster than other features

- Transaction volume doubled in 2024

- Lower average transaction value indicates daily usage

- Rewards Platform

- 185B+ monthly coin burn

- Lower DAU/MAU indicates periodic engagement

- Strong correlation with bill payment cycles

The data shows CRED successfully maintaining engagement in core credit card payments while growing rapidly in UPI transactions, though with smaller transaction sizes indicating changing usage patterns.

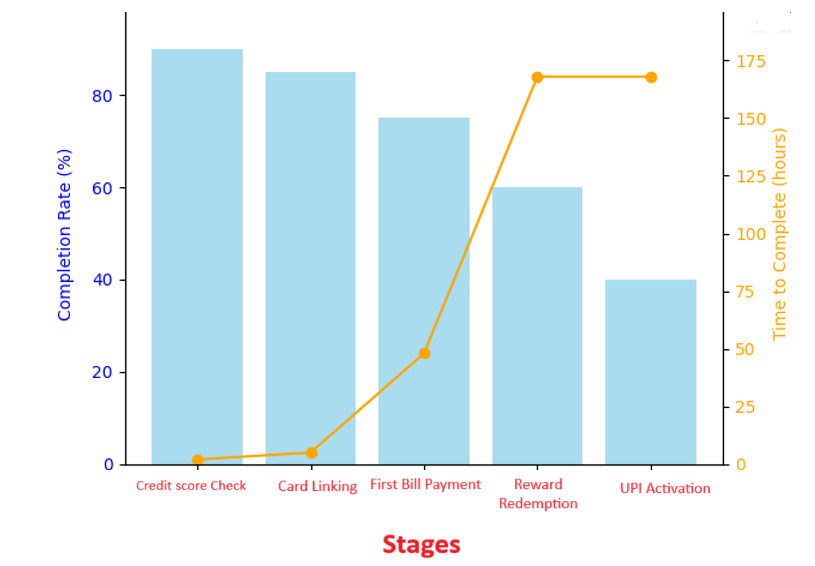

3.Time to activation per feature

Feature | Time to Activation | Completion Rate |

|---|---|---|

Credit Score Check | 1-2 minutes | 90% |

Card Linking | 3-5 minutes | 85% |

Bill Payment | 24-48 hours | 75% |

Rewards Redemption | 5-7 days | 60% |

UPI Activation | 5-7 days | 40% |

Key insights taken from above:

- Initial onboarding (credit check + card linking) typically completed within first 10 minutes

- Core payment functionality activated within 48 hours

- Reward ecosystem engagement peaks around week 1

- UPI adoption follows successful bill payment experience

- Higher activation rates for core features vs auxiliary services

The data shows strong early engagement with core features, while auxiliary features like UPI and rewards see delayed but steady adoption patterns over the first week of usage.

4.User journey completion rates

Based on the graph, here's an analysis of CRED's user journey completion rates and timelines:

User Journey Timeline

Quick Completion Features (0-24 hours)

- Credit Score Check: 90% completion in 2 hours

- Card Linking: 85% completion in 5 hours

Medium-Term Features (24-72 hours)

- First Bill Payment: 75% completion in 48 hours

Long-Term Features (1 week+)

- Reward Redemption: 60% completion in 168 hours (7 days)

- UPI Activation: 40% completion in 168 hours (7 days)

Key Insights

- Highest completion rates correlate with core onboarding features

- Sharp decline in completion rates for optional features

- Clear inverse relationship between time to complete and completion rate

- UPI activation shows lowest completion rate despite being a key feature

- Initial engagement (first 24 hours) shows strongest user participation

Quality Metrics

- Payment success rates

- App stability metrics

- Overall Stability Score: ~99.63% (industry median)

- Error-free Experience: Above 99% for core features

- User satisfaction scores

- App Store Rating: 4.1/5

- User Satisfaction Rate: ~70% based on active user engagement and also product reviews states so.

- Monthly Active Users: 13 million

These hypotheses and metrics help track CRED's success in converting high-quality users while maintaining its premium positioning and users.

Brand focused courses

Great brands aren't built on clicks. They're built on trust. Craft narratives that resonate, campaigns that stand out, and brands that last.

All courses

Master every lever of growth — from acquisition to retention, data to events. Pick a course, go deep, and apply it to your business right away.

Courses

Built by Leaders From Amazon, CRED, Zepto, Hindustan Unilever, Flipkart, paytm & more

Crack a new job or a promotion with ELEVATE

Designed for mid-senior & leadership roles across growth, product, marketing, strategy & business

Learning Resources

Browse 500+ case studies, articles & resources the learning resources that you won't find on the internet.

Patience—you’re about to be impressed.